A drug receives regulatory approval. Clinical trial results are strong. Physicians are interested. Investors are optimistic.

Yet one year after launch, patient adoption remains far below expectations.

The product struggles to secure formulary access. Health Technology Assessment (HTA) agencies question its value proposition. Pricing negotiations delay reimbursement decisions. Physicians face prescribing restrictions. Patients encounter access barriers.

This is not a clinical failure.

It is a market access failure.

Pharma market access is the discipline responsible for ensuring that approved medicines reach patients at a price healthcare systems are willing to reimburse. It combines health economics, pricing strategy, reimbursement planning, payer engagement, patient support, and evidence generation.

For pharmaceutical companies, market access is no longer a post-approval activity. It has become a strategic function that influences development decisions years before launch.

Organizations that begin market access planning during Phase 2 consistently achieve faster reimbursement, broader patient access, and stronger commercial performance than those that wait until approval.

The Problem: Clinical Success Does Not Guarantee Commercial Success

The gap between regulatory approval and patient access is growing wider. Several structural factors explain this.

Payer scrutiny is increasing. HTA bodies (NICE in the UK, G-BA in Germany, HAS in France) apply stricter evidentiary standards.

Pricing pressure is global. International reference pricing means the price in one country affects what you can charge elsewhere. The IRA introduces Medicare price negotiation.

Formulary restrictions are tightening. Even with approval, step therapy, prior authorization, or restricted placement reduces patient reach.

According to IQVIA Institute, approximately 50% of pharmaceutical launches in 2020-2024 underperformed commercial forecasts, with market access barriers as the primary factor.

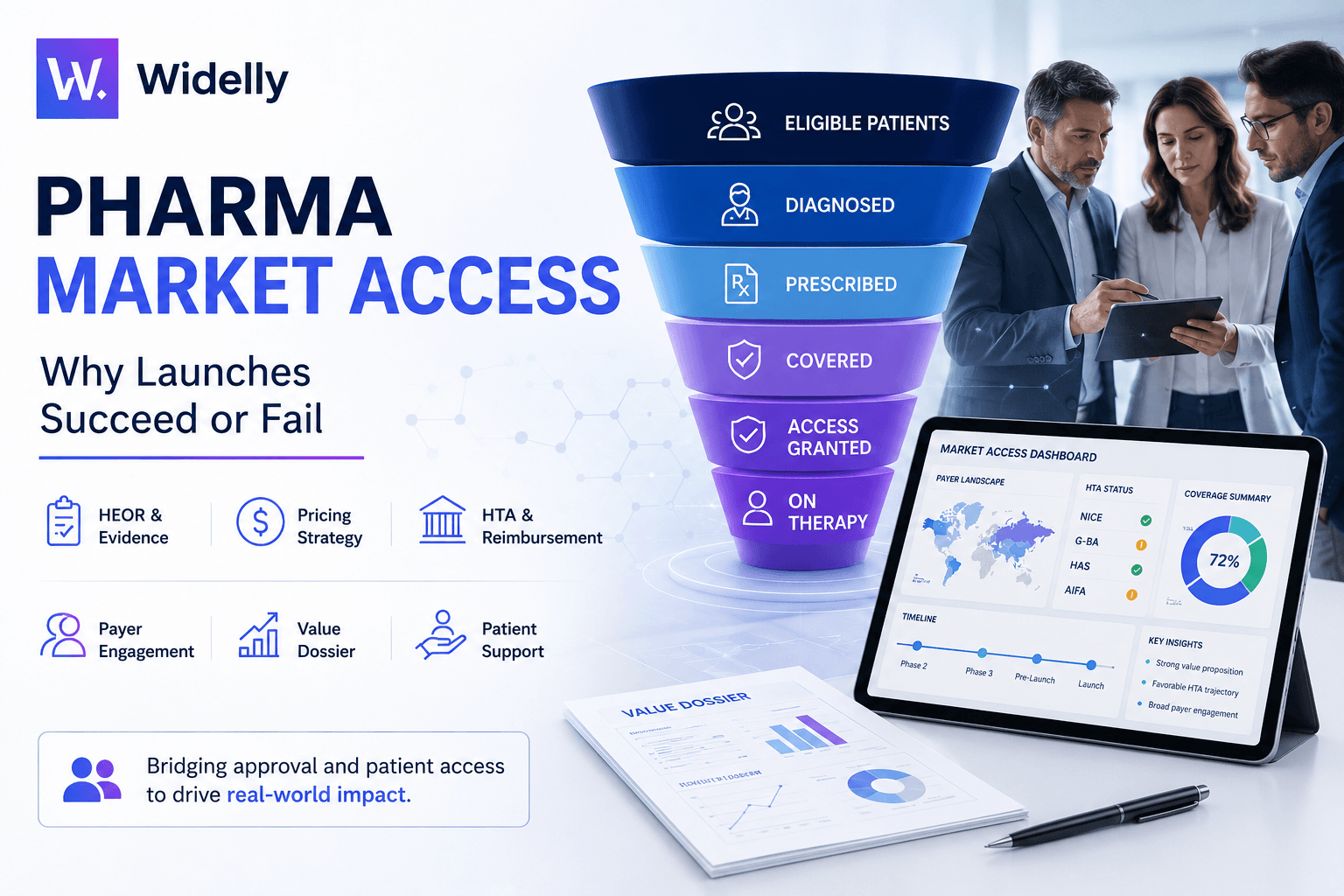

Patient Access Funnel

Even successful launches reach only 22% of eligible patients in Year 1

The Insight: Market Access Is Not Just Pricing

The most common misconception is that market access is primarily about pricing. It encompasses everything that determines whether an approved drug reaches patients at a sustainable price.

| Component | What It Covers | When It Matters |

|---|---|---|

| HEOR | Clinical and economic evidence for payers | Starts in Phase 2 |

| Pricing strategy | Global architecture, reference pricing, net vs. list | 18-24 months pre-launch |

| HTA/Reimbursement | NICE, G-BA, HAS submissions | 12-18 months pre-launch |

| Value dossier | Evidence package for payer justification | 12-18 months pre-launch |

| Payer engagement | Formulary committees, managed care | 18+ months pre-launch |

| Patient support | Hub services, co-pay, specialty pharmacy | 6-12 months pre-launch |

The real insight: Companies that consistently achieve strong market access start planning 3-5 years before launch – during Phase 2. Companies that begin after approval are already behind.

Decision Intelligence: Why Launches Fail – Five Patterns

| Failure Pattern | Root Cause | Prevention Timing |

|---|---|---|

| Wrong evidence | Clinical program not designed with payer endpoints | Phase 2 trial design |

| Single-market pricing trap | No global pricing architecture | 24+ months pre-launch |

| HTA misalignment | Value story not calibrated to HTA frameworks | 18 months pre-launch |

| Formulary delays | Late engagement with payer review processes | 12+ months pre-launch |

| Patient access barriers | Inadequate patient support infrastructure | 6-12 months pre-launch |

The Solution: Market Access Planning Timeline

Market Access Planning Timeline

The Value: What Good Market Access Delivers

Early vs. Late Market Access Planning

Early

3 months

Late

9 months

Early

45%

Late

22%

Example: Two Launches, Same Indication, Different Outcomes

Two companies launch in the same rare disease indication within 6 months.

Company A begins market access in Phase 2. They conduct payer advisory boards, learn that payers want functional outcome data, add a secondary endpoint, engage NICE early scientific advice, and set global pricing 24 months pre-launch. Result: positive NICE recommendation, broad access, Year 1 revenue exceeds forecast by 15%.

Company B focuses on clinical development. Market access starts 12 months pre-approval. Their data lacks functional outcomes. They submit to NICE without early advice. Result: restricted recommendation, US price undercut by reference pricing. Year 1 revenue is 35% below forecast.

The clinical data was comparable. The market access planning was not.

Understanding NICE and Global HTA Reviews

NICE remains one of the most influential HTA organizations globally.

The standard appraisal process often requires:

- Evidence submission

- Economic evaluation

- Committee review

- Stakeholder consultation

The process may take 12–18 months.

Other HTA agencies follow similar principles, although methodologies differ by country.

Successful companies tailor submissions to local requirements rather than applying a single global approach.

Market Access Trends to Watch

Several trends are reshaping pharmaceutical market access.

Inflation Reduction Act (IRA)

The IRA continues to influence pricing strategy and lifecycle planning.

Real-World Evidence

Payers increasingly expect evidence beyond clinical trials.

Value-Based Agreements

Outcome-linked reimbursement contracts continue to expand.

AI-Driven Evidence Generation

Artificial intelligence is improving evidence analysis and economic modeling.

Patient-Centered Outcomes

Patient-reported outcomes are becoming increasingly important during reimbursement reviews.

Organizations that adapt early will be better positioned for future reimbursement success.

Conclusion

Market access bridges the gap between regulatory approval and patient access.

Clinical success alone is no longer sufficient.

Organizations must demonstrate value to payers, HTA agencies, healthcare systems, and patients.

The most successful pharmaceutical companies begin market access planning years before launch.

They integrate payer requirements into clinical development, build strong economic evidence, engage stakeholders early, and prepare reimbursement strategies long before approval.

For commercial leaders, market access is no longer a support function.

It is a strategic capability that directly influences revenue, patient reach, and long-term product success.

In today’s environment, the question is not whether market access matters.

The question is whether organizations are investing early enough to realize its full value.

Frequently Asked Questions

What is market access in pharma?

Market access is the process of securing reimbursement, pricing approval, and patient access for pharmaceutical products after regulatory approval.

When should market access planning begin?

Most experts recommend beginning market access planning during Phase 2 development to ensure evidence generation aligns with payer expectations.

How is market access different in the US and Europe?

The US relies on payer negotiations with insurers and PBMs, while European countries typically use formal HTA organizations to determine reimbursement decisions.

What is HEOR?

Health Economics and Outcomes Research (HEOR) evaluates the clinical and economic value of therapies to support reimbursement decisions.

What is a value-based contract?

A value-based contract links reimbursement levels to real-world clinical outcomes achieved by patients.

Why do pharmaceutical launches fail despite approval?

Common reasons include insufficient payer evidence, reimbursement delays, pricing challenges, formulary restrictions, and patient access barriers.

What is NICE?

The National Institute for Health and Care Excellence (NICE) is the UK’s HTA organization responsible for evaluating the clinical and economic value of healthcare interventions.

Why is market access important for commercial success?

Market access determines whether approved therapies receive reimbursement, gain formulary access, and ultimately reach patients at scale.

Related Topics

About the Author

Hamza

Healthcare Market Research and Business Development Specialist with a strong focus on pharmaceutical, biotech, and life sciences sectors. Experienced in analyzing market trends, competitive landscapes, and growth opportunities to support strategic decision-making. Skilled in transforming complex healthcare data into actionable insights that drive business expansion, partnerships, and revenue growth.

Related Articles

How AI Is Changing Clinical Trial Design in 2025

A CMO reviews a Phase 2 protocol. The team has designed a traditional randomized, double-blind,…

China Biotech Licensing Wave: What It Means for Western BD Teams

In 2023, Chinese biotechs signed over $50 billion in total deal value with Western pharma…

Decentralized Clinical Trials: Benefits, Limitations and When to Use Them

During the pandemic, a Phase 3 trial for a cardiovascular drug shifted from 100% site-based…